Autor

Viljar Vald, CFA

Kuupäev

29/01/2026

Our inaugural year in live markets showed a close alignment between our models and actual trading results. The strategy transitioned with minimal friction to deliver solid performance, confirming the integrity of our approach in real-world conditions.

Executive Summary

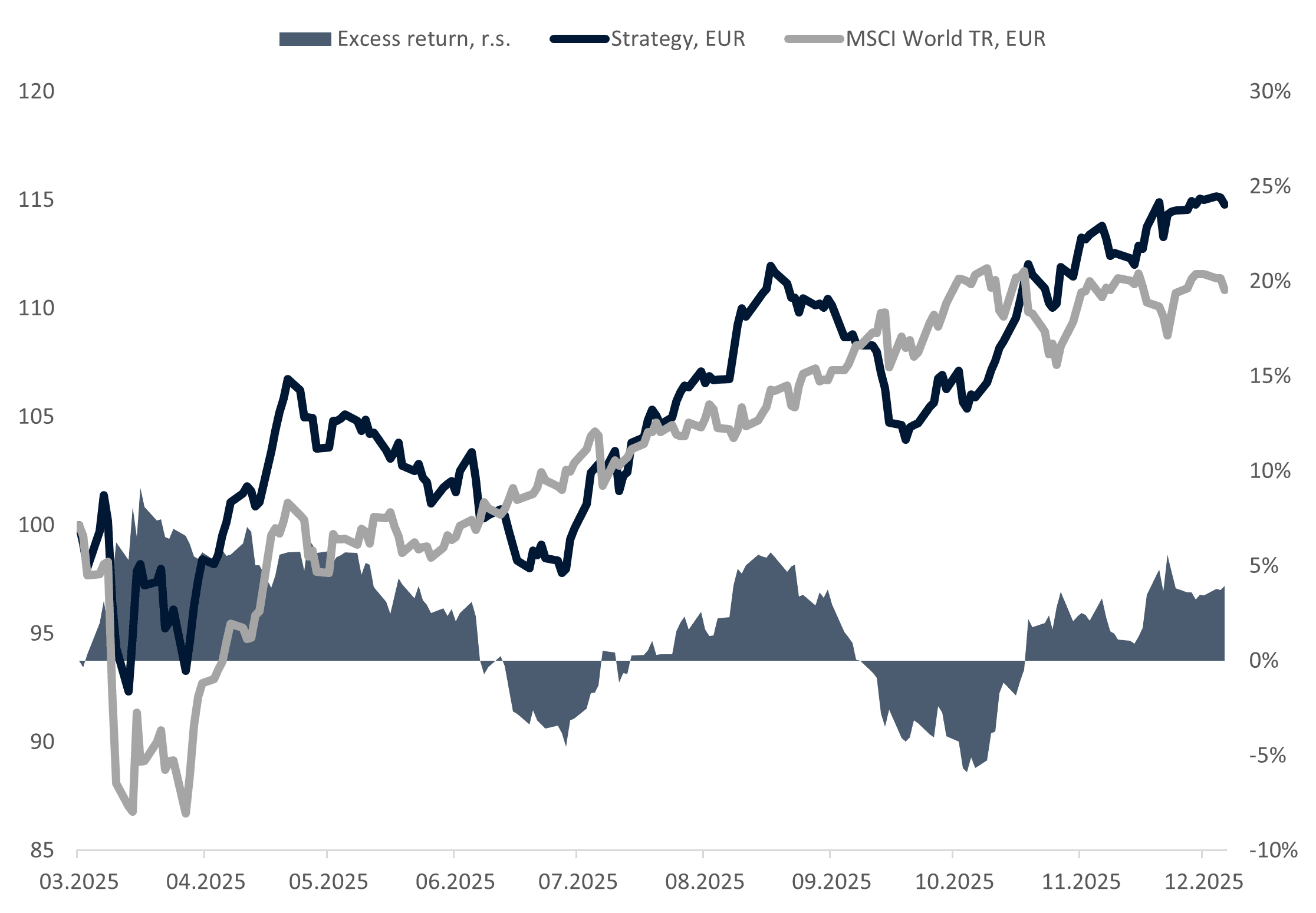

• Performance: The strategy delivered a +14.8% net return EUR (+25.2% USD) from inception (March 26, 2025) through year-end, outperforming the benchmark (MSCI World) by 395 bps.

• Risk Profile: Captured outperformance with a realized market beta of 0.5, providing significant capital protection during deleveraging events.

• Architecture: A 200/100 active extension structure, maintaining a diversified book of approximately 1,500 positions across liquid stocks in developed global markets.

• High Model Fidelity: Successfully transitioned from theoretical backtest to live markets with 97.9% realized correlation and 2.8% tracking error, confirming minimal implementation leakage and robust strategy adherence.

Part I: Performance & Strategic Rationale

The 2025 Market Environment

The 2025 investment landscape was characterized by significant macro uncertainty and punctuated market volatility. While the global equity benchmark ultimately ended the year with strong gains of 21% in USD terms and only 6.8% in EUR terms,[1] the path was anything but linear. Investors navigated sharp deleveraging events and shifting macro narratives that tested the resilience of traditional equity portfolios.

Chart 1. Cumulative returns since inception

Source: Sarto Capital Management calculations.

Within this environment, Sarto Capital Management’s systematic global equity strategy was launched on March 26, 2025. Our objective was not merely to track the market's upward momentum, but to build an efficient equity portfolio capable of navigating volatility spikes without sacrificing growth. The strategy’s year-end result of +14.8% EUR, (+25.2% in USD) represents not just a gain in capital, but a validation of our systematic framework’s ability to extract both beta and alpha under varying market conditions. With a realized beta of only 0.5, the strategy effectively captured more than 9% of alpha during the approximately 9-month period.

Table 1. Comparative statistics

Source: Sarto Capital Management calculations.

Capital Efficiency: The 200/100 Structure

Our strategy utilizes a 200/100 Active Extension framework. This means the portfolio is a fully integrated long short structure, which maintains a 100% net-long exposure to the equity market.

This structure allows us to:

1. Harvest Factor Premia: We don't just "own the market"; we use the long/short extension to extract returns from the price gap between high-quality and low-quality equities over the long term.

2. Maintain High Breadth and Diversification: With approximately 1,500 positions, we avoid idiosyncratic single-stock risk. Our performance is a function of repeatable factor exposures, not luck.

3. Ensure Liquidity: We focus exclusively on the liquid global segments, with majority of the exposure in liquid large-cap equities, ensuring the strategy remains scalable and execution robust.

Defensive Tilt: 100% Net Market Exposure with Beta Less than 1

The strategy is designed to be 100% net long to participate in the market’s long-term growth, while maintaining an effective beta of less than 1.0. This decoupling allows the portfolio to capture additional systematic premia with less dependency on broad market direction. By prioritizing defensive factors, the strategy achieves volatility and drawdown levels similar to or slightly lower than the global equity benchmark, despite embedded leverage. This was evidenced by strategy’s lower realized volatility and drawdown than the benchmark in 2025.

Part II: Technical Performance & Risk Appendix

Note for Technically Oriented Readers: The following section provides a more granular look "under the hood" of the strategy’s engine.

The goal of a robust track record is to demonstrate two things: (i) that backtested results effectively transfer to live portfolios, and (ii) that the strategy can endure different market regimes.

1. Factor Resilience: Defensive Alpha in Volatile Regimes

Over its initial nine months, the strategy "fortunately" encountered two distinct market regimes: a volatility spike and market sell-off during "Liberation Day" (April 2025), followed by a subsequent "junk" rally. This scenario serves as a rigorous test for any long/short strategy, as correlations typically spike during the initial shock, and the short book can become a drag in the ensuing low-quality rally.

The strategy’s primary risk-mitigation tool is its inherent defensive factor tilt. Unlike strategies that rely on expensive non-linear hedges, Sarto Capital harvests "Flight-to-Safety" alpha through its structural preference for high-quality, resilient equities.

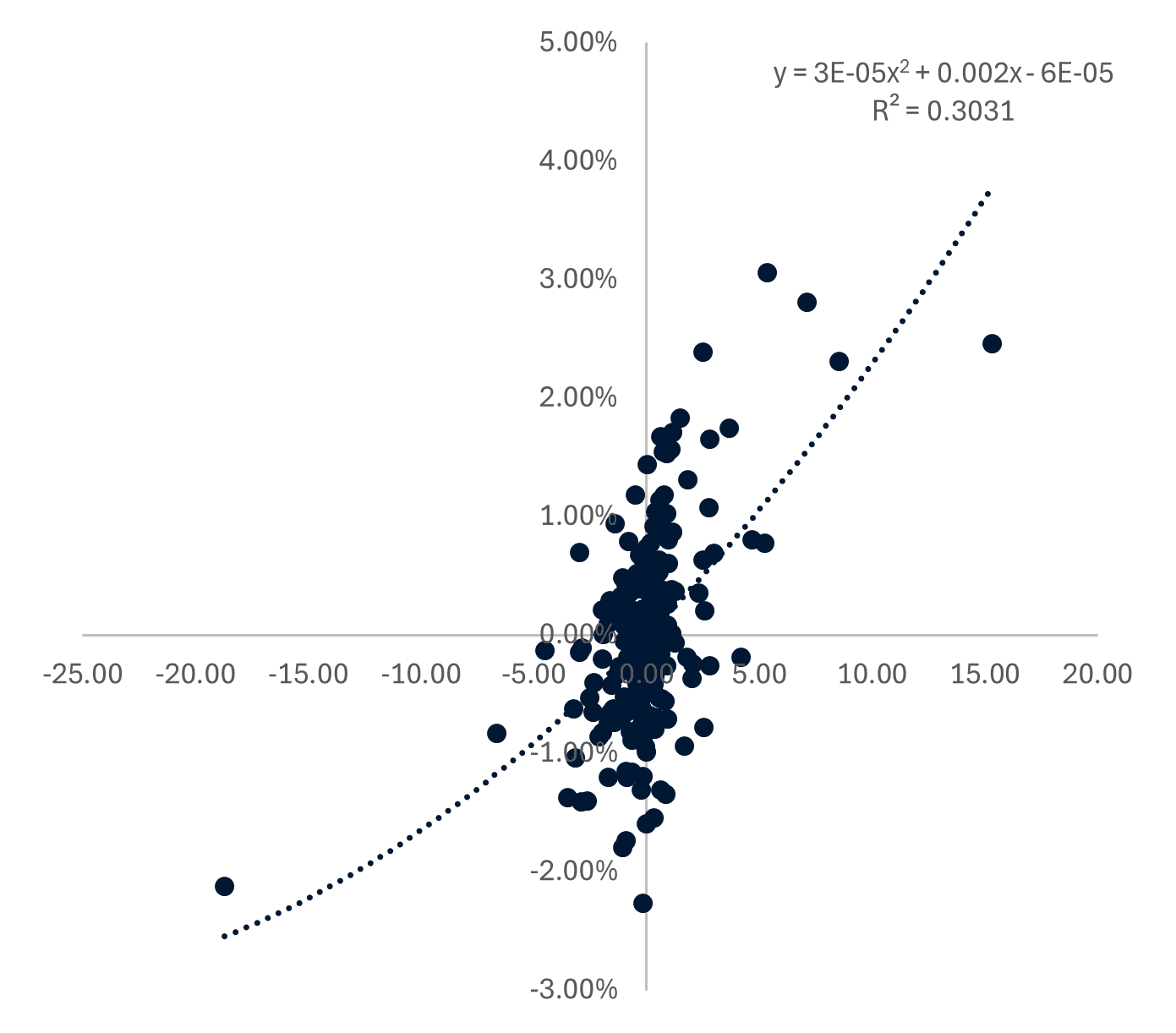

· Realized Performance: During market deleveraging events — such as the volatility spikes observed in April 2025 — the strategy demonstrated a down-capture ratio of less than 50%.

· VIX Sensitivity: We observed a positive excess return correlation to VIX. This was not achieved through derivatives, but structurally through the systematic selection of stocks with superior balance sheets and stable earnings, which historically have tended to decouple from the broader index during liquidity crunches. This effectively „long volatility“ profile mitigates drawdowns during market shocks without the need for expensive tail-risk hedging.

Chart 2. Strategy daily excess return (y-axis) & VIX daily level change (x-axis)

Source: Sarto Capital Management calculations.

2. Execution Integrity & Inception Risk

To address the inception risk common to new strategies, we meticulously tracked the performance of our theoretical model and live execution.

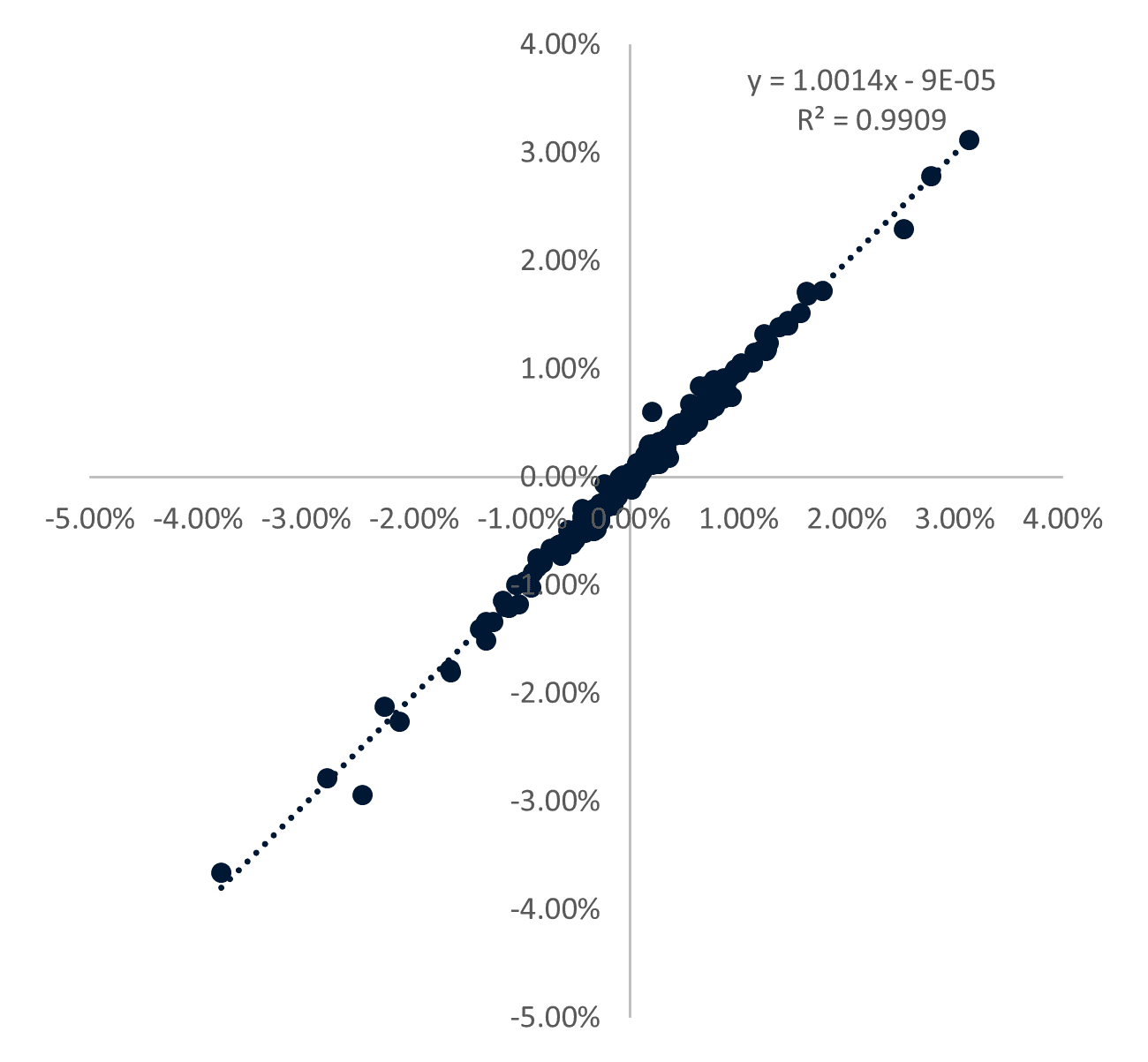

· High Correlation: We recorded a 97.9% correlation between daily model returns and actual realized returns, effectively mirroring theoretical model results in the actual portfolio.

· Low Replication Error: The annualized tracking error of daily return differences (model vs. actual) was only 2.8%.

· Liquidity and Friction: Results confirm all the execution frictions, including trade commissions, slippage, short book borrow costs and other frictions are well-contained and within estimated limits. Because we trade only the most liquid global segments, our execution remains robust, providing a high-integrity reflection of our underlying logic as we scale.

Chart 3. Daily model returns (x-axis) vs actual portfolio returns (y-axis)

Source: Sarto Capital Management calculations.

Part III: Outlook — An All-Weather Vehicle for 2026 & Beyond

As we look toward 2026 and beyond, we believe the investment landscape is likely to move from a strongly beta-driven era to a more disperse, selection-driven era. The extreme concentration currently observed at the index level suggests that passive returns may be more subdued moving forward, while simultaneously providing significant opportunities for active, systematic managers to add value.

A Unified Approach to Equity Investing

Our strategy is designed as an All-Weather vehicle suited for this transition. By effectively and efficiently capturing both Beta and Alpha, we offer a rational alternative to traditional equity exposure:

· Capturing Market Returns Effectively: With a beta of less than 1.0, we participate in the market's long-term upward trajectory but with a stabilizer that mitigates the impact of sharp corrections.

· Capturing Alpha Efficiently: Our 1,500-position breadth allows us to harvest returns from stock-level dispersion. In stagnant or volatile markets where passive index returns may disappoint, our ability to extract value from the spread between "long" and "short" selections becomes the primary driver of growth.

In conclusion, Sarto Capital Management remains focused on the operational and systematic discipline that defined 2025. We believe the coming cycle will reward strategies that can deliver consistent results across all market environments by prioritizing risk management and structural alpha.

[1] MSCI World Net Total Return EUR Index

General disclaimer

The information on this site is provided for general informational purposes only. Nothing on this site constitutes, or is intended to constitute, an offer to sell or market any interest in any investment opportunity. It also does not constitute an advertisement of, or an offer to provide, any investment management or advisory product or service.

Regulatory status

Sarto Capital Management OÜ is registered with the Estonian Financial Supervision Authority (Finantsinspektsioon) as a small alternative fund manager. However, it is not an authorised fund manager and is not subject to ongoing supervision by the Estonian Financial Supervision Authority.