Author

Viljar Vald, CFA

Date

27/11/2025

Markets are trading near all-time highs. Anything with “AI” in its name is soaring, and FOMO is back in full force. At moments like these, it’s worth asking whether an all-out offensive in equities is really the best long-term game plan.

We live in a time when new technologies are expected to transform both society and the economy, and the companies behind them are assumed to deliver profits on a similar scale. On the back of this narrative, for example, OpenAI's valuation has risen to around 500 billion dollars, even though its cash flows are still negligible and it faces capital expenditures in the hundreds of billions that will need to be earned back many times over in the future.

The dream of spectacular equity returns and the fear of missing out can easily lead to questionable investment decisions. That is why it is worth recalling an old but still valid idea: the best offense is often a strong defense. In investing, that does not mean sitting in cash, but allocating capital to companies with resilient business models, strong balance sheets and stable profitability. This is what investors call quality, and history shows that quality is one of the few approaches that has proved its value time and again.

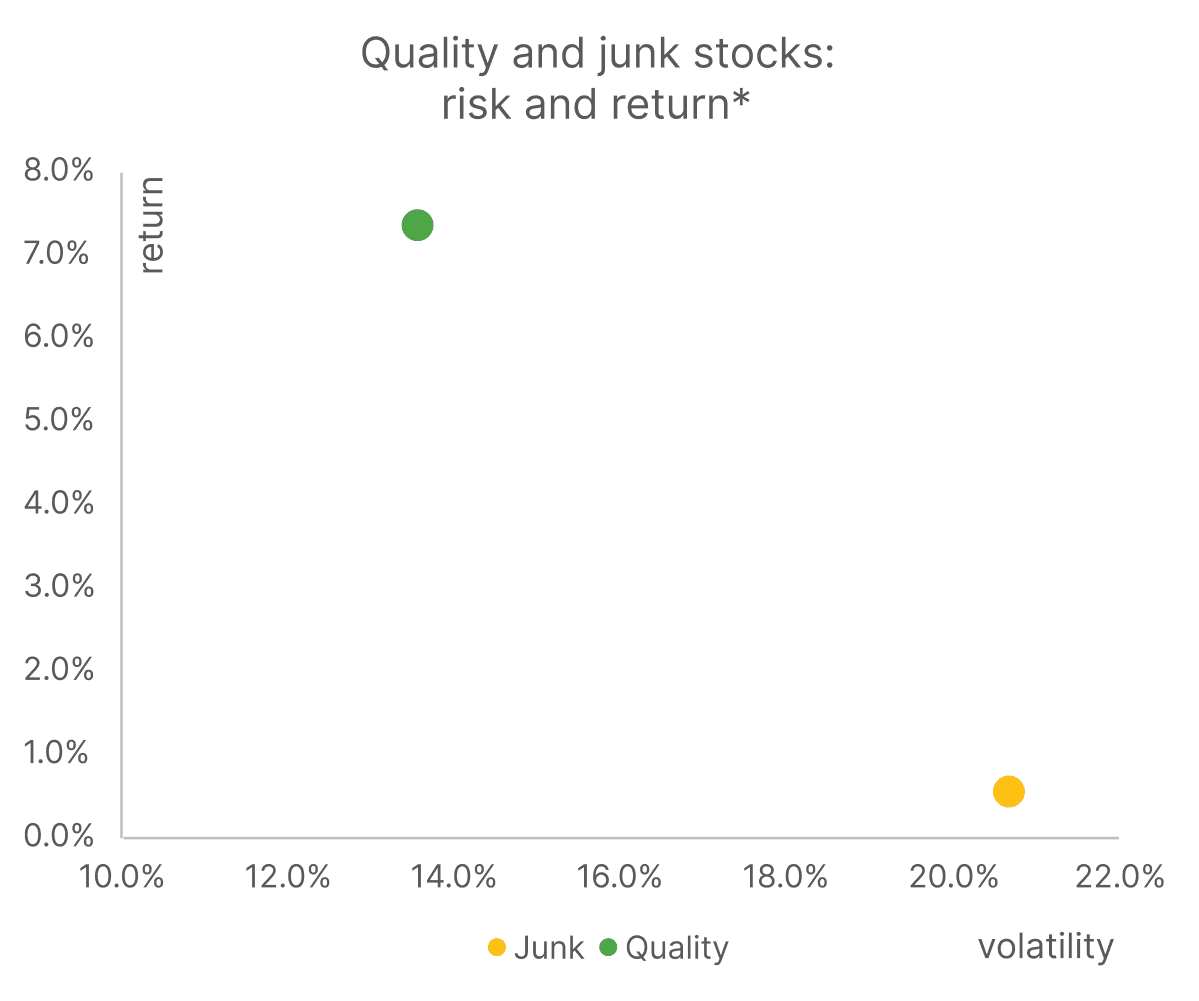

It’s long been a cornerstone of finance that higher returns come with higher risk. That principle holds up well across asset classes. For instance, stocks tend to outperform bonds over time, but within the stock market, things get more interesting. History shows that companies with solid balance sheets, steady profitability, and moderate leverage often deliver higher risk-adjusted returns than their flashier, more volatile peers.(1) Academics call this the “low-risk anomaly.”

* Quality and Junk are defined as the top quintile (20%) vs bottom quintile of stocks based on ranking. AQR data, global stocks 1989-2025, annualized return and volatility; Sarto Capital Management calculations

What drives this anomaly?

If riskier stocks are supposed to offer higher returns in theory, why does the opposite so often happen in practice? Economists have studied this question, and the answer seems to lie in investors’ constraints and psychology.

First, most investors simply don’t have the ability to use leverage. If they can't boost returns by borrowing, they try to do it by buying higher-risk stocks instead.(2),(3) The problem is, those stocks get bid up too far compared with their steadier, “boring” counterparts. Over time, the quiet performers come out ahead.

Second, there’s the behavioral explanation or the so called “lottery effect”.(4),(5) A slim chance of an outsized win just feels more exciting than a predictable but modest gain. You see the same thing in sports betting, where people can't resist the long shot. In equity markets, this implies that investors systematically overpay for highly speculative "pie-in-the-sky" type of stocks while undervaluing more stable, consistent companies.

Last but not least, investors are influenced by their incentives.(6) Many of the professional investors’ career and pay outcomes are dependent on short term market outperformance. The advantage of quality stocks tends to become evident mainly during weak markets, when they decline less in downturns but also lag in rallies. Because markets rise more often than they fall, many investors likely don’t find that defensive edge attractive enough.

What defines a quality stock?

The quality factor isn’t just another passing trend. It reflects a durable, structural advantage. You see it in the resilience of business models, the consistency of profits and the efficient use of capital. Yet markets often undervalue these kinds of companies, favoring short-term excitement over long-term strength.

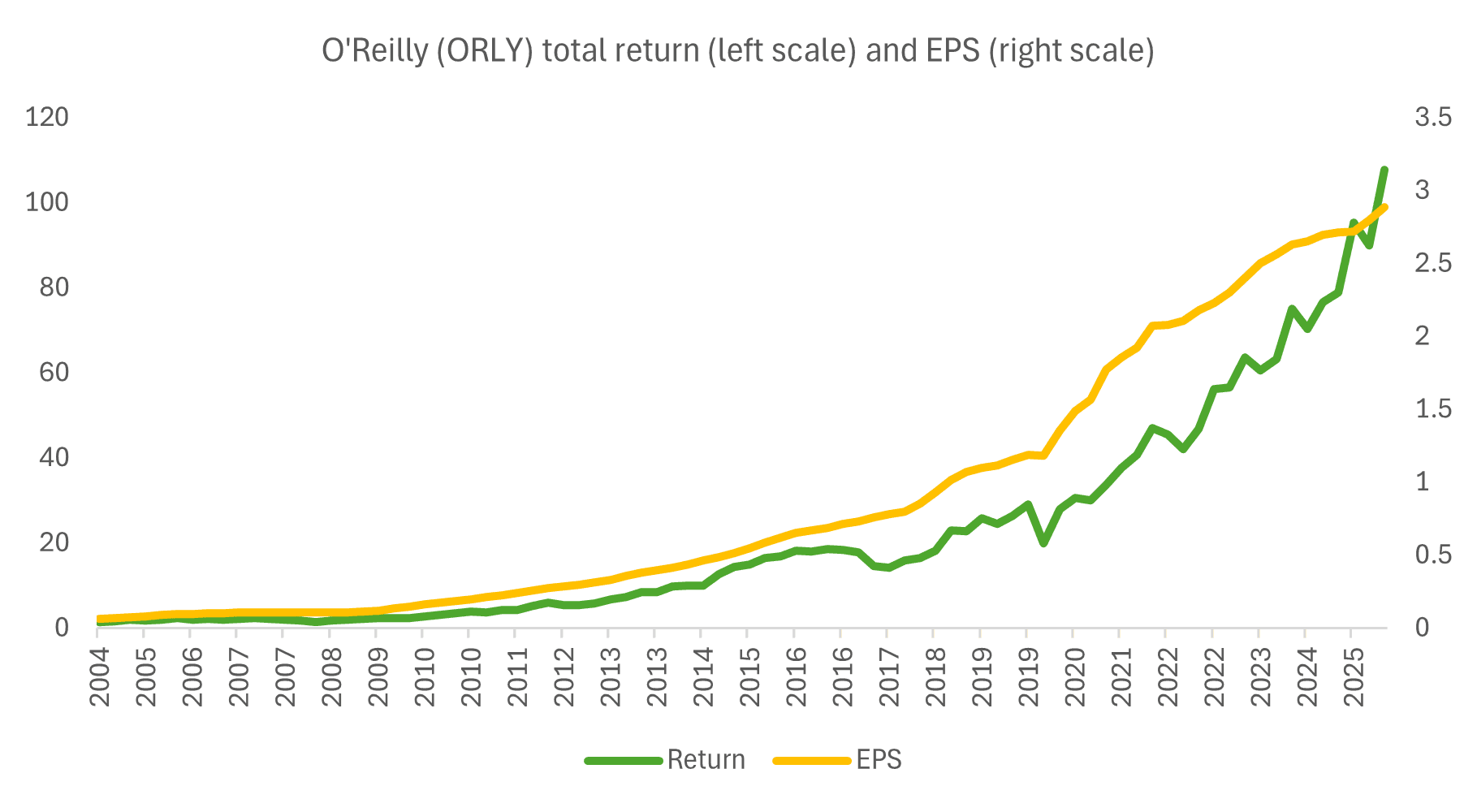

Consider O’Reilly Automotive, a U.S. auto parts retailer. It’s not a glamorous business, but over the past two decades it has grown earnings by about 15% a year and delivered more than 20% average annual returns to shareholders. O’Reilly isn’t a market superstar, but it perfectly represents the kind of business that anchors the quality factor: steady, profitable and often underestimated. In the market’s eyes, it’s “boring” but in reality, it’s one of the most effective engines for compounding capital.

Source: Bloomberg, Sarto Capital Management calculations

A systematic approach over intuition?

Quality works best when applied systematically across hundreds or even thousands of companies to build a diversified portfolio. Think of the market as a haystack. The systematic quality strategy doesn’t look for just one single needle, but focuses on the part of the stack where the needles are most likely to be found. Simple, transparent and grounded in solid economics, this approach has proven far more resilient than the opaque “black box” models that come and go with each market cycle.

The same systematic logic can also be applied on the other side of the market by shorting unattractive stocks. Short positions can enhance portfolio returns by adding an additional source of income and helping to cushion losses in market downturns, since they tend to generate profits when prices fall. At the same time, managing a portfolio of short positions effectively is complex, costly and demanding, which makes it unrealistic for most individual investors and is better left to professionals.

Systematic and quantitative approaches are often dismissed as a kind of “black box”, where complex algorithms search past data for patterns that may not repeat in the real world. And there is truth to this concern. Many such strategies do fall short of their promises once they are applied in live markets. Every so often a new approach is promoted, sometimes based on new data, sometimes on a new method. The latest fad is AI-based stock selection. Most of these ideas do not live up to the expectations placed on them, especially those that are widely marketed to the general public.

For that reason, it is important that the signals a strategy relies on are simple, economically sensible and supported by long histories in different markets and asset classes. Strictly speaking, we are talking about tendencies rather than certainties, because in financial markets we always deal in probabilities, not guarantees. When a tendency is persistent and shows up in many places, it is more likely to reflect a durable feature of markets than a temporary anomaly or a passing trend.

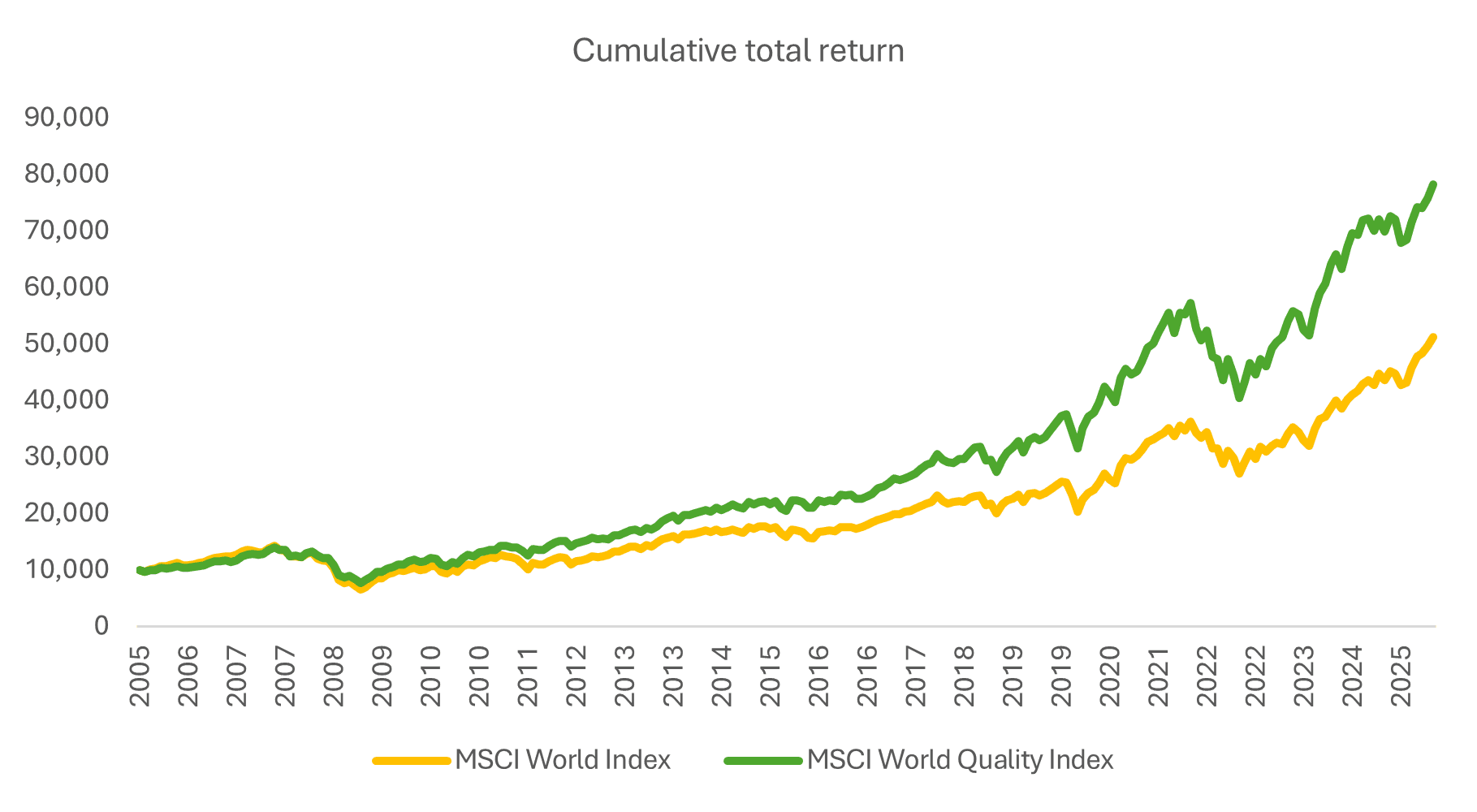

The data supports this. Over the past twenty years, the MSCI World Quality Index has outperformed the broader MSCI World Index by roughly two percentage points per year – and all this with lower volatility. Compounded over time, the difference becomes substantial: an investment of €10 000 made in 2005 would have grown to about €50 000 in the market index, or nearly €80 000 in the quality-focused one.

Source: Bloomberg, Sarto Capital Management calculations

Long-term consistency

Academic and industry studies have found similar patterns.(7),(8) Quality-based portfolios have delivered stronger returns in the United States, Europe, Japan and emerging markets alike. The advantage over a broad market index is not dramatic in any single period, but its strength and persistence mean that, if structured properly, it can provide noticeable additional returns over time.

Quality rewards patience. It pays off over time, though not necessarily every quarter or even every year. At times, other factors take the lead and quality temporarily falls behind. That isn’t a flaw but a natural part of the cycle, one that helps sustain its long-term advantage. In the end, the strength of quality lies not in pushing forward aggressively, but in holding the line.

Quality as a long term strategy

Quality is, in a way, both defense and offense. It is defensive because quality companies usually fall less in crises. It is offensive because they tend to preserve earnings and capital, and can take advantage of opportunities created when others have taken on too much risk. Quality works somewhat like an insurance policy that does not require paying a premium, because it can generate its own return over time.

There are periods when high-risk stocks pull far ahead of more defensive, “boring” companies. At such times, it is tempting to abandon the strategy. But investment decisions should not be guided by whatever happens to be in vogue. The focus should stay on a process that is logical, repeatable and tested over time. Quality is one such process. It does not rely on a single market or a lucky break, but on discipline, both from companies and from investors.

In the short term, quality can feel dull, even a drag, when markets are racing ahead. But when the noise fades and fundamentals matter again, as they eventually do, it is usually the “boring” companies that stay afloat. From time to time, a few risky stocks will become genuine superstars, but as a group they tend to be poor investments, because very few investors can identify the long-term winners in advance. Quality is not only a form of protection against risk; it is also a highly effective way to turn risk into an advantage over the long run.

The article has also been published here: https://arvamus.postimees.ee/8368185/viljar-vald-parim-runnak-on-kaitse-kvaliteet-aktsiaturul

References:

(1) Clifford S. Asness & Andrea Frazzini & Lasse Heje Pedersen, 2019. "Quality minus junk," Review of Accounting Studies, Springer, vol. 24(1): 34-112

(2) Frazzini, Andrea & Pedersen, Lasse Heje, 2014. "Betting Against Beta," Journal of Financial Economics, vol. 111(1): 1-25

(3) Jylhä, Petri & Rintamäki, Paul, 2021. „Leverage Constraints Affect Portfolio Choice: Evidence from Closed-End Funds,“ SSRN, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3722010

(4) N. Barberis & M. Huang, 2008. „Stocks as Lotteries: The Implications of Probability Weighting for Security Prices,“ American Economic Review, Vol 98(5): 2066-2100

(5) Brunnermeier, Markus K. & Christian Gollier & Jonathan A. Parker, 2007, "Optimal Beliefs, Asset Prices, and the Preference for Skewed Returns," American Economic Review, vol. 97(2):159-165

(6) Chretien, S, Coggins, F, Deslauriers, C, 2025. “Tournament effects in equity mutual funds: Impact of economic conditions and investment styles,” The Journal of Financial Research

(7) Lepetit, F., Cherief, A., Ly Y., Sekine, T., 2021 „Revisiting Quality Investing“. SSRN: https://www.researchgate.net/publication/352837230_Revisiting_Quality_Investing

(8) Ilmanen, A., 2022 „Investing Amid Low Expected Returns: Making the Most When Markets Offer the Least,“ 1st Edition, Wiley Publishing